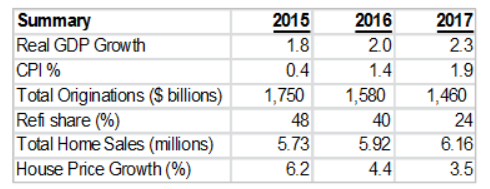

Mortgage pool funds are benefitting from the increased demand for fix-and-flip loans that has accompanied the robust housing market of recent months. Housing was an especially bright spot in the economy last year and is shaping up to be a growth area again in 2016. The continued imbalance between supply and demand for both houses and apartments supports higher home prices and rents and demand exceeding supply will remain a factor driving increased home prices this year, according to the Federal Home Loan Mortgage Corporation (Freddie Mac). Rent growth is also expected to remain above average levels. Freddie Mac also believes that persistent low mortgage rates will facilitate home purchases, although refinance volume may begin to decline later this year due to Fed monetary tightening and rising interest rates.

A significant demographic trend boding well for continued vigor in the housing market is a surge in demand from millennial home buyers. Millennials are loosely defined as Americans who were born between 1980 and 1996. The millennial generation has already surpassed Generation Xers as the largest share of the U.S. workforce and became America’s largest living generation last year. Although millennials aren’t yet fully immersed in the housing market, their impact will be enormous in the next few years.

Millennials Lead All Home Buyers

At 32 percent, millennials made up the largest share of home buyers in 2015. More importantly, they represented 68 percent of all first-time home buyers, according to the National Association of Realtors. A TD Banks survey suggests that the number of millennial home buyers will begin to accelerate since nearly half of the millennials surveyed said they expect to purchase their first home within the next two years. Compared to earlier generations, millennials are more inclined to believe that home ownership is a smart investment. Their optimism may be due to the fact that, unlike their parents, millennials weren’t directly impacted by the 2008 housing market collapse.

The sheer size of this demographic has major implications for future housing markets. Economists expect millennials to form approximately 24 million new households over the next decade. Their impact on the housing market was delayed because, until a few years ago, large numbers of millennials were still living with their parents. In 2012, a Pew Research study showed that 11 million recent college graduates were living with their parents and home ownership by young adults was at its lowest level since 2005. As the job market has gradually improved, however, more millennials have entered the housing market. Retiring baby boomers are creating better job opportunities for millennials and their increased salaries allow them to become more focused on home ownership. Most millennials earn enough to afford a home. Studies show median income for this group is $73,600.

More Than One Million New Households Forming Annually

Another factor fueling the housing boom by millennial buyers is rising rents, which make home ownership a more attractive option than renting. According to Time.com, nearly 60 percent of U.S. housing markets are expected to raise rents over the next few years to levels sufficiently high to make home ownership more affordable than renting.

Also, the majority of millennials are entering their prime marriage and household-forming years. College-educated people are the group most likely to own homes and the millennial generation has the largest percentage of college graduates in U.S. history. The prime marriage age for college-educated Americans is 25-26 and the largest sub-group of millennials (i.e. those born after 1990) is reaching that age. Marriage and new household formation is expected to spur housing market demand for the next several years. A Goldman Sachs analyst who covers the housing sector recently predicted that single-family housing starts will nearly double to 1.1 million a year by 2019.

Some analysts worry that rising interest rates could stymie millennial buyers, but that is unlikely for several reasons. First, even if interest rates inch up, mortgage rates are still unusually low by historical standards. Second, Fed rate adjustments mainly affect short-term rates, and mortgage rates are more correlated with longer-term rates, which are dictated by market forces. In addition, there is another group of Americans re-entering the housing market that will compete with millennials to purchase homes. They are former home owners who declared bankruptcy or defaulted on their mortgage during the housing crisis. More than seven years have passed since the crisis and these former home owners now have a clean credit slate and renewed purchasing power.

Migration Westward to the Suburbs

A noteworthy trend among millennial buyers is migration from the city to the suburbs. A survey by the National Association of Home Builders found that nearly two-thirds of millennials plan to look for single-family suburban homes even if they currently live in the city. Millennials are also more likely than other generations to hire a real estate agent to help them find their dream home.

Regarding geographic distribution, a survey by the National Association of Realtors indicated that many millennials are looking to move West and Midwest. The prime markets for millennial buyers are Austin, Dallas, Denver, Des Moines, Grand Rapids, Minneapolis, New Orleans, Ogden, Salt Lake City and Seattle.

Opportunities for “Fix-and-Flip” Homes

Millennial buyers are more willing than other demographic groups to invest in home upgrades. A 2014 survey by Better Homes and Gardens showed that, as a group, millennials were the least likely to buy a newly constructed home (18 percent) and the most likely to purchase a fixer-upper (23 percent). Among millennial home owners planning a home improvement project in the next twelve months, nearly 35 percent agreed that “now is the right time” to make home improvements. Among all the millennial home owners surveyed, 45 percent said they were planning or have begun a major home improvement project.